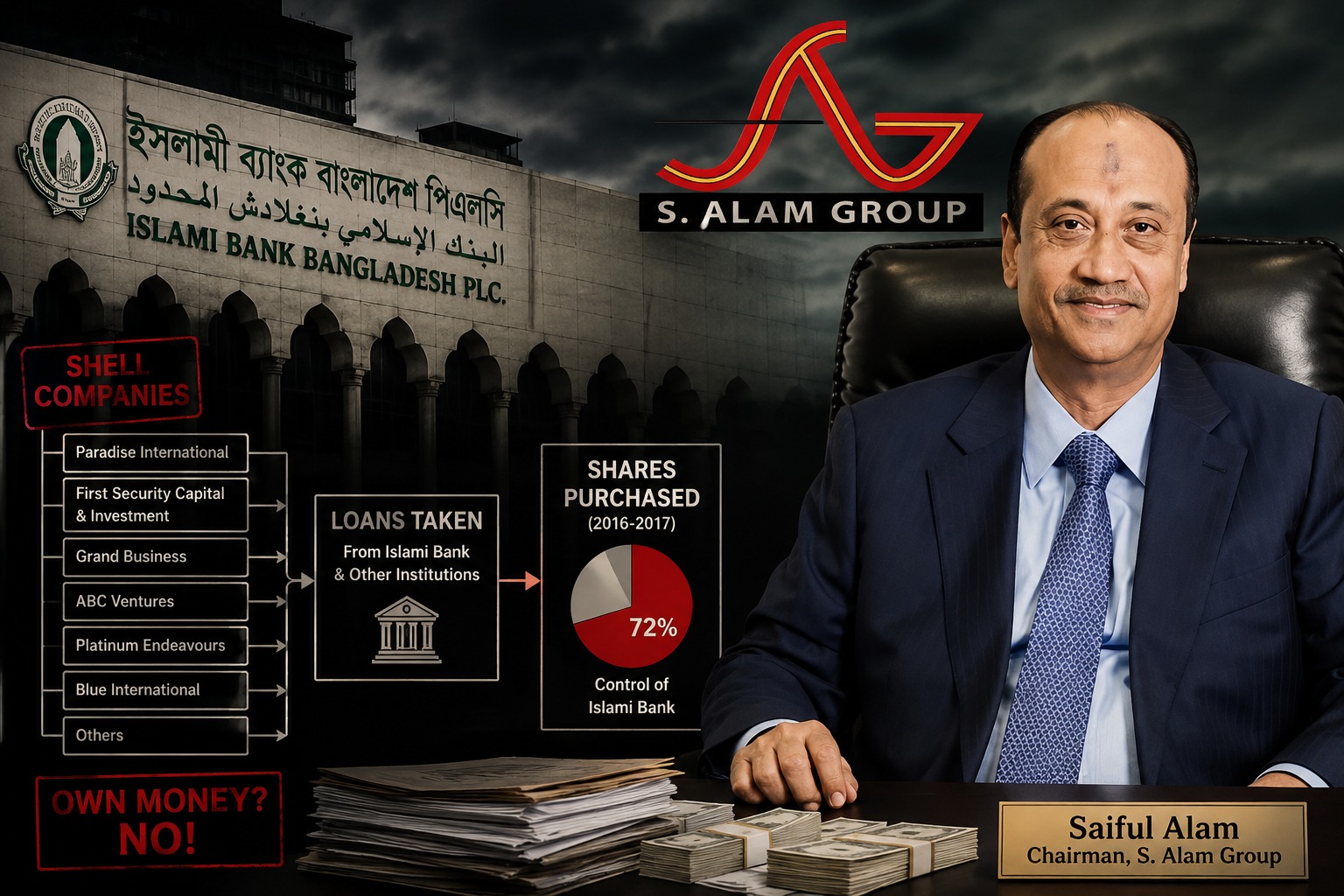

S Alam Group did not acquire control of Islami Bank Bangladesh PLC with its own money. Instead, according to an investigation by the Bangladesh Financial Intelligence Unit (BFIU), the conglomerate allegedly used funds originating from the bank itself and from other financial institutions already under its influence.

The findings, submitted before the High Court, paint a picture of a sophisticated financial scheme in which loans were channelled through a network of shell companies and proxy shareholders to purchase a controlling stake in Bangladesh’s largest Islamic bank.

According to the BFIU, between 2016 and 2017, S Alam Group gradually accumulated approximately 72 percent of Islami Bank’s shares through 22 proxy shareholders and a series of suspected shell entities. The acquisition was allegedly financed largely through loans obtained from Islami Bank and several other financial institutions controlled by the group.

Once control of the bank was secured, the flow of funds allegedly reversed direction. Ownership of the bank enabled the group to access even larger credit facilities, strengthening its influence across the financial sector and creating what experts describe as a classic case of regulatory capture where a private business group uses financial institutions and regulatory weaknesses to consolidate economic power.

The BFIU report suggests that the takeover was not merely a corporate acquisition but a coordinated effort that allowed the conglomerate to leverage the banking system’s own resources to finance its expansion. During this period, regulators, including Bangladesh Bank and the Bangladesh Securities and Exchange Commission (BSEC), either failed to intervene or did not detect the irregularities.

Seven Companies at the Centre of the Share Acquisition

Investigators found that seven companies linked to S Alam Group played a central role in the initial acquisition of Islami Bank shares.

One of them, Paradise International, purchased shares worth approximately Tk 71.33 crore. According to the investigation, the funds were traced back to accounts belonging to S Alam Super Edible Oil maintained with First Security Islami Bank. Part of the financing was routed through entities including Momentum Business Center, Epic Able Traders, Invention Trade International, Abdul Awal & Sons (Patiya), Nabir Trading and Existence Trade Agencies companies identified by investigators as either affiliated entities or shell companies.

Another major shareholder, First Security Capital & Investment, acquired 64.3 million shares through the account of Excel Dyeing & Printing. The transaction was reportedly financed through Sonali Traders, S Alam Super Edible Oil and S Alam Refined Sugar Industries. Investigators identified company directors linked to close relatives of S Alam Group Chairman Mohammed Saiful Alam.

Similarly, Armada Spinning Mills purchased 33.7 million shares using funds allegedly channelled through S Alam Super Edible Oil, S Alam Vegetable Oil and S Alam Refined Sugar Industries, alongside financing from Green Expose Traders, which the BFIU identified as a shell company.

Other entities including Grand Business, ABC Ventures, Platinum Endeavours and Blue International also acquired substantial blocks of shares. Investigators traced their financing back to various S Alam Group companies and associated entities, many of which later emerged among the bank’s largest loan defaulters. The report notes that several directors and shareholders of these companies were either relatives of Saiful Alam or individuals with direct links to businesses controlled by the group. Foreign Shareholders Under Scrutiny The BFIU also found evidence suggesting possible links between S Alam Group and two foreign companies that acquired shares in Islami Bank. Investigators identified the involvement of a company secretary from an S Alam-affiliated entity in one of the transactions involving foreign shareholders. Based on these findings, the BFIU suspects that the group's effective ownership in Islami Bank may have reached as high as 81.92 percent. The agency has recommended a broader and deeper investigation to determine the full extent of the group's involvement. High Court Questions Legality of Ownership Structure The High Court has already issued a rule questioning how 24 entities came to hold 81.92 percent of Islami Bank's shares and why those holdings should not be confiscated. The court has also ordered restrictions on dividend distribution, suspension of voting rights attached to the disputed shares, and the freezing of relevant bank accounts pending further proceedings. In its report submitted to the court, the BFIU stated that its conclusions were based on an extensive review of banking records, loan documents, transaction vouchers, approval letters and account information obtained from Islami Bank, First Security Islami Bank, Global Islami Bank, Union Bank and several capital market intermediaries. The investigation concluded that approximately 72.07 percent of the bank’s shares were linked directly or indirectly to individuals and entities associated with S Alam Group. Loans Used to Buy the Bank One of the most significant findings of the investigation is the apparent overlap between the entities that financed the share purchases and the bank’s largest loan defaulters. According to Islami Bank’s records, 15 of its top 20 defaulting borrowers are linked to S Alam Group, its chairman Saiful Alam, his son Ahsanul Alam, son-in-law Belal Ahmed and other family members. S Alam Super Edible Oil, identified as one of the principal sources of funds used during the share acquisition, is now the bank’s largest defaulting borrower with outstanding classified loans of Tk 13,040 crore. Other major defaulters include: S Alam Refined Sugar Industries Tk 10,281 crore S Alam Vegetable Oil Tk 10,113 crore Sonali Traders Tk 4,853 crore Chemon Ispat Tk 3,592 crore Several of these companies were directly involved in financing the purchase of Islami Bank shares, raising serious concerns about whether the bank’s own lending facilities were ultimately used to facilitate its takeover. Legal and Regulatory Implications Senior Supreme Court lawyer Barrister Abdul Qayyum, who represents the petitioner in the case, argues that the acquisition violated Bangladesh’s banking laws. Under existing regulations, no individual or business group may hold more than 5 percent of a bank’s shares without regulatory approval, and even with approval, ownership is generally capped at 10 percent. “S Alam Group acquired more than 72 percent of Islami Bank in violation of Sections 14 and 15 of the Bank Company Act,” he said. Former Bangladesh Bank Deputy Governor Rumee Ali noted that proving the true source of funds will be central to any legal challenge. “Even if the shares are not registered directly in S Alam’s name, ownership can be challenged if it is proven that the funds originated from entities under the group’s control,” she said. She further argued that courts should summon the nominal shareholders and require them to disclose the beneficial owners behind the shares. Providing false information under oath could constitute perjury and carry serious legal consequences. Meanwhile, Bangladesh Bank has stated that the matter remains sub judice and that any regulatory action will depend on the court’s findings. If the allegations are ultimately proven, the case could become one of the most significant examples of alleged corporate capture and banking sector abuse in Bangladesh’s history raising fundamental questions about governance, regulatory oversight and accountability within the country’s financial system.